This Is Fine

Both the U.S. economy and the U.S. consumer are on shaky footing

In today’s post, we'll quickly look at three warning signs for the stock market…

The 'Magnificent 7' continues to drive the majority of the market’s performance

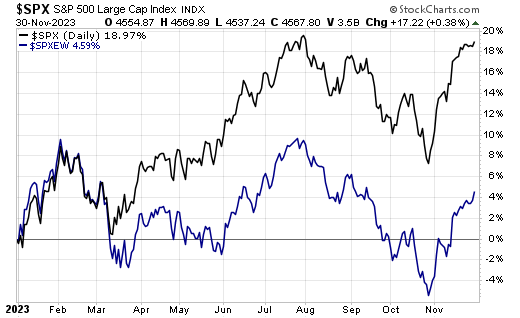

At the surface, the blue-chip S&P 500 Index is humming along nicely this year, up 19% as of last week.

But the S&P 500 is weighted based on market cap. That is, the bigger a company gets, the bigger its representation in the S&P 500.

The so-called "Magnificent 7" stocks — Alphabet (GOOGL), Amazon (AMZN), Apple (AAPL), Meta Platforms (META), Microsoft (MSFT), Nvidia (NVDA), and Tesla (TSLA) — comprise a staggering 28% of the index's weighting today.

These stocks are up an average of 102% year to date, with Apple's 47% returns somehow the laggard of the bunch.

The S&P 500 Equal Weight Index tells a different story… This index is equally divided by all 500 companies. So solar panel maker SolarEdge (SEDG) and its $4.5 billion market cap is weighted the same as Apple and its $3 trillion market cap.

While the S&P 500 is up 19% this year, the equal weight index is up just 4.6%. Take a look:

When (not if) these stocks take a breather from their tremendous rally this year, it will pull the rest of the market lower with them… potentially, a lot lower.

Warren Buffett is selling stocks and sitting on cash

Every quarter, investors take a close look at the portfolio of Berkshire Hathaway's (BRK) Warren Buffett.

Buffett, largely considered the greatest investor of all time, is he's famous for the following quote:

"Our favorite holding period is forever."

Yet, the Oracle of Omaha sold a net $8 billion worth of stock last quarter, liquidating positions in General Motors (GM) and "defensive" stocks like Johnson & Johnson (JNJ), Procter & Gamble (PG), and Mondelez (MDLZ).

Buffett is also sitting on a record $157 billion in cash right now:

He’s sitting in cash because he knows a storm is brewing in the markets, which will give him an opportunity to buy high-quality stocks at a discount. That brings me to the third (and most worrisome) warning sign…

The U.S. consumer is hurting

I could write thousands of words about this last topic, and it's one I plan to address more in future posts. But for now, consider the following…

According to Adobe, Black Friday spending in the U.S. hit a record $9.8 billion, an 8% increase from last year, while Cyber Monday sales hit a record $12.4 billion. And yet, nearly $800 million of that was made with buy now, pay later services like Klarna and Affirm. That's up almost 20% from the same time last year.

A recent report from Intuit showed that an incredible 96% of Americans are concerned about the U.S. economy right now, but more than a quarter of them are "doom spending."

That jives with the latest travel data from TSA, which said that 2.9 million people passed through U.S. airports on the Sunday after Thanksgiving, the busiest day of travel in history.

The U.S. consumer continues to buy, but he's putting it on his credit card… Credit card debt recently exceeded $1 trillion. Americans are paying an average interest rate of 28% on that.

Total household debt — including credit cards, mortgages, and auto and student loans — sits at $17 trillion. Meanwhile, data from Bankrate shows that more than one in five Americans has no money set aside for an emergency.

But if things look so wobbly for the economy and the consumer, why shouldn’t you wait on the sidelines for a year or two to see how things shake out with the stock market?

As I explained in my last post, “time in the market beats timing the market.” Nobody can predict exactly when the market will take a nosedive.

There’s never a bad time to buy world-class, cash-gushing businesses with wide moats and long histories of returning cash to shareholders — as long as you’re buying them at reasonable prices.

Or as the recently departed Charlie Munger was known for saying, “A great business at a fair price is superior to a fair business at a great price.”

Sure, stocks may tumble, and you probably won’t end up bottom-ticking every stock you buy.

And if you’re a retiree living on a fixed income who can’t afford to take losses, that’s another story altogether… But if you have money to invest that you don’t need for the next, say, decade, you should always have a chunk of it in stocks.

The best stocks will weather the next storm, just as they always do. That’s why, despite my generally bearish macro stance right now, I still think it’s a great time to buy great businesses.

In my next posts, I’ll start to do a mini dive into some of my favorite companies right now. Some are household names trading at reasonable valuations. Others are lesser-known and more cyclical in nature, but they offer tremendous upside and limited downside nonetheless.

Be sure to subscribe so you never miss a post.

Hi Sam! Herb gave you a nice shoutout and I’m curious about your newsletter!

> The U.S. consumer continues to buy, but he's putting it on his credit card… Credit card debt recently exceeded $1 trillion. Americans are paying an average interest rate of 28% on that.

Unless I’m severely mistaken, this number includes all credit card debt, including the debt within the grace period before interest accumulates. The vast majority of credit card holders pay their balances on time and don’t incur any interest costs.

It’s always nice to put any amount into perspective by providing a suitable denominator, ie divide credit card balances by disposable income or nominal GDP. When you do that you get a very different picture.

Bob Elliott and Lyn Alden have done that kind of analysis on twitter and I recommend their work.

You had me at the dog in the fire meme :)